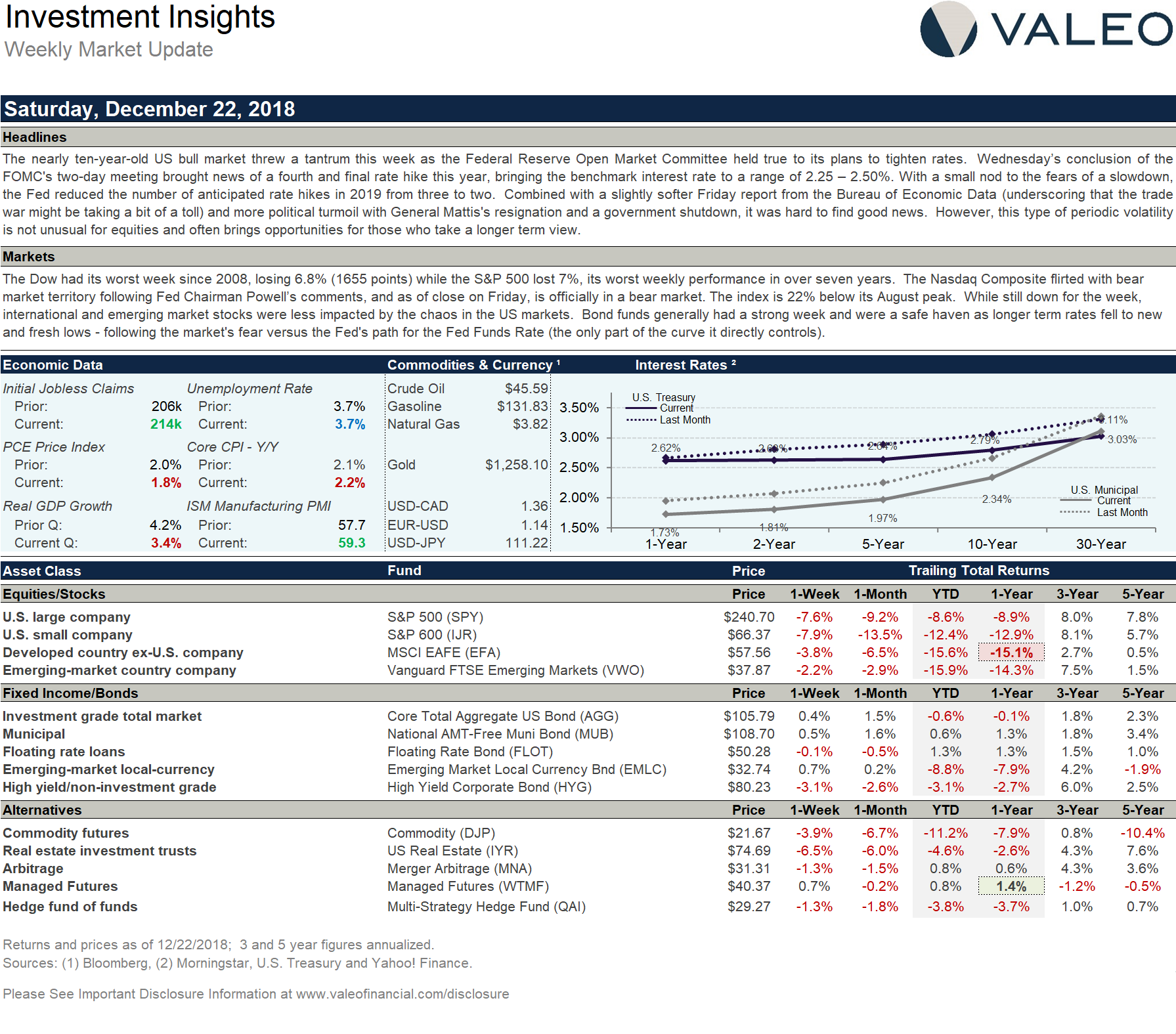

The nearly ten-year-old US bull market threw a tantrum this week as the Federal Reserve Open Market Committee held true to its plans to tighten rates. Wednesday’s conclusion of the FOMC’s two-day meeting brought news of a fourth and final rate hike this year, bringing the benchmark interest rate to a range of 2.25 – 2.50%. With a small nod to the fears of a slowdown, the Fed reduced the number of anticipated rate hikes in 2019 from three to two. Combined with a slightly softer Friday report from the Bureau of Economic Data (underscoring that the trade war might be taking a bit of a toll) and more political turmoil with General Mattis’s resignation and a government shutdown, it was hard to find good news. However, this type of periodic volatility is not unusual for equities and often brings opportunities for those who take a longer term view.

The Dow had its worst week since 2008, losing 6.8% (1655 points) while the S&P 500 lost 7%, its worst weekly performance in over seven years. The Nasdaq Composite flirted with bear market territory following Fed Chairman Powell’s comments, and as of close on Friday, is officially in a bear market. The index is 22% below its August peak. While still down for the week, international and emerging market stocks were less impacted by the chaos in the US markets. Bond funds generally had a strong week and were a safe haven as longer term rates fell to new and fresh lows – following the market’s fear versus the Fed’s path for the Fed Funds Rate (the only part of the curve it directly controls).

Click on image below for larger view.